Public Comps - Jan '20 SaaS Multiples & Bill.com

2020 SaaS Multiples & 2019 IPO Review & Bill.com Teardown

👋From Jon and Howard 👋

Happy 2020! Thank you for being supporters of Public Comps. We’re offering a special promotion for new customers. If you apply “ilovesaas” at checkout, you’ll get 50% off your first month of Public Comps!

Key Takeaways

1️⃣SaaS Multiples: 2020 has gotten off to a nice start for public SaaS companies. For all SaaS companies, Median EV/NTM ARRR (annualized revenue run rate) is 8.8x up from the low of 7.3x in September 2019 and the low of 5.8x in December 2018. For the highest growth SaaS companies (top decile), median EV/NTM ARRR is 12.8x down from the high of 18x in July 2019.

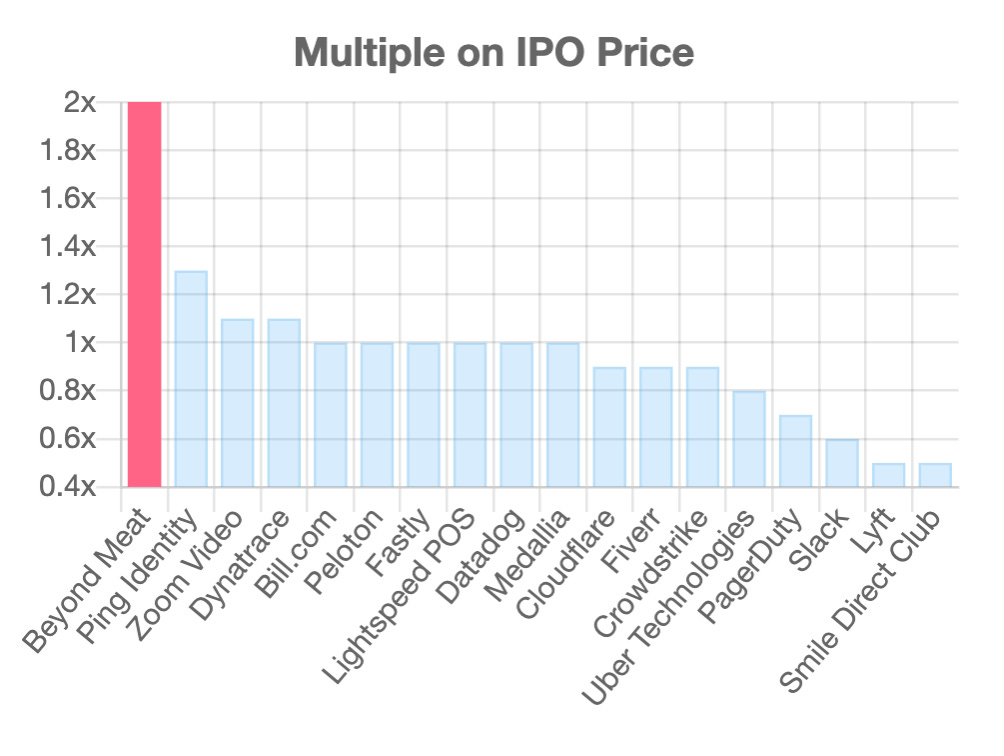

2️⃣2019 IPO Reviews: Most 2019 IPOs ended up trading at 1x their IPO price. Biggest gains are Beyond Meat (2x), Ping Identity (1.3x), biggest losses are Smile Direct Club (0.5x), Slack (0.6x), and Uber (0.8x). Interesting that it's a mix of both consumer and enterprise with big wins and losses.

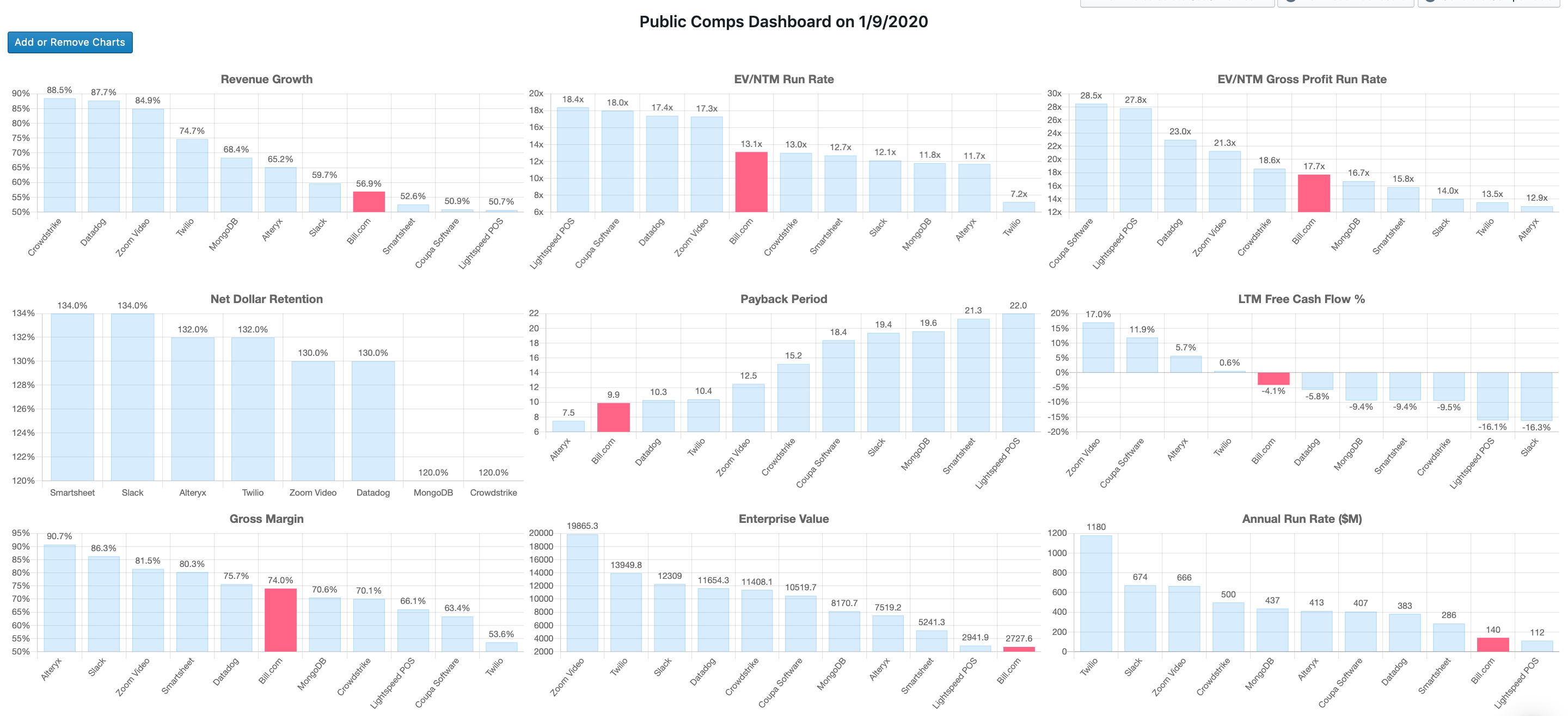

3️⃣Bill.com IPO: Bill.com went public in December '19 and is a software company that's moving SMB payment online and growing quickly. However, the valuation is quite rich relative to peers and doesn't have exceptional metrics other than payback period as calculated by taking the inverse of CAC Ratio and has been around for over 13 years.

🙋♂️We'd love feedback & chat: https://calendly.com/jonbma/30min

Public SaaS Multiples - January 9th, 2020

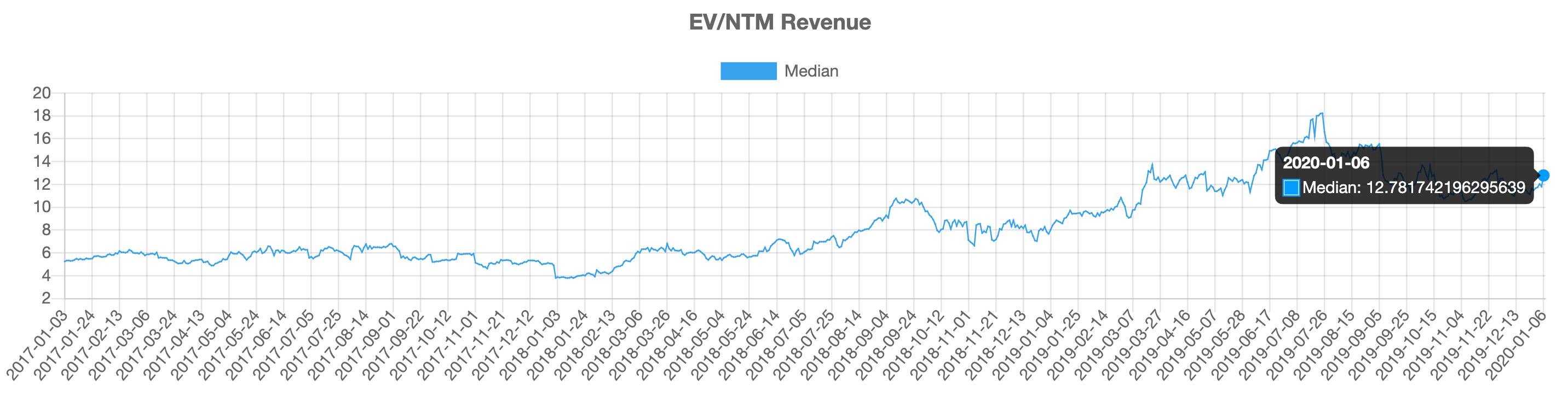

High growth SaaS

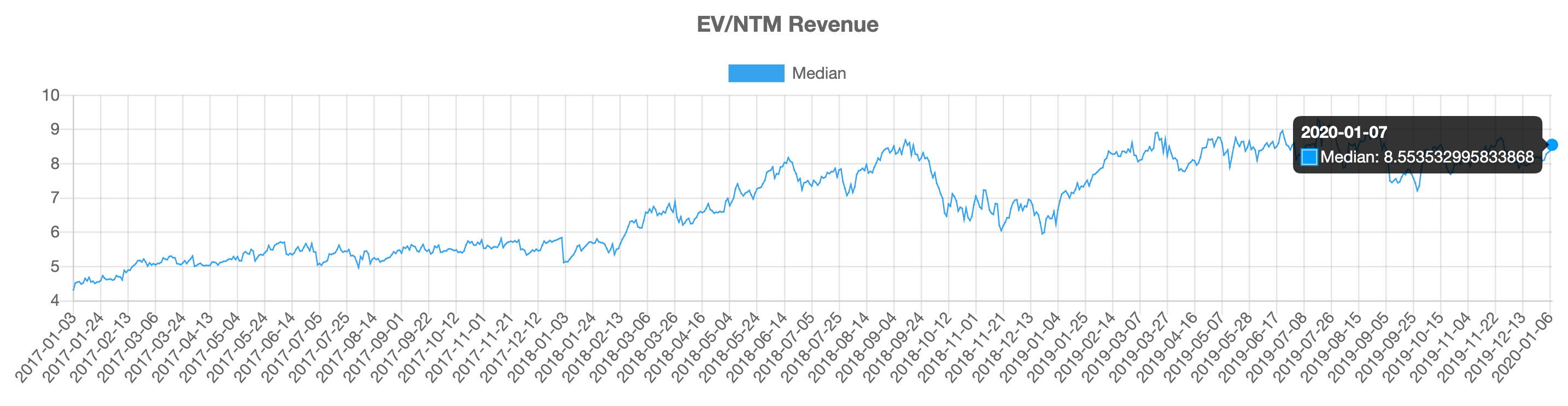

All SaaS Companies

👉Takeaway: SaaS multiples are up to start 2020. Median EV/NTM ARRR is 8.8x up from the low of 7.3x in September 2019 and the low of 5.8x in December 2018. For the highest growth SaaS companies (top decile), median EV/NTM ARRR is 12.8x down from the high of 18x in July 2019.

2019 IPO Review

📈2018 was the year of high-growth SaaS IPOs and 2019 didn't disappoint with the IPO of Zoom, Crowdstrike, Slack, Fastly, Datadog, Dynatrace, Cloudflare, among others. Zoom and Crowdstrike soared out of the IPO gates in mid-2019 with their 100% YoY growth rates and then their stock prices plunged in Q3'19 amidst fears that software buying was slowing down (⁇) and that the companies were highly overvalued.

It's worth reiterating why a company like Zoom trades for nearly 17.3x and, say, Uber trades for 3x--Zoom was growing 100%+YoY and now at 85% while demonstrating it can generate real cashflow with nearly 30% FCF margins in its most recent quarter. Whereas Uber is growing 30% YoY with -26% FCF (-$1B of cash burned in Q3'19). Zoom has an efficiency of nearly 115% and Uber 3.5% -- the Rule of 40 matters.

That said, the winner of the 2019 IPO is Beyond Meats which is a producer of plant-based foods growing 250% with -20% FCF margins at nearly 2x their IPO opening price. Time will tell how these companies fare overtime.👉Takeaway: Most 2019 IPOs are still trading at 1x their IPO price. The biggest gains are Beyond Meat (2x), Ping Identity (1.3x) and biggest losses are Smile Direct Club (0.5x), Slack (0.6x), and Uber (0.8x). Interesting its a mix of both consumer and enterprise with big wins and losses.

Bill.com Dec'19 IPO Teardown

👉 See the Publiccomps.com Benchmarks live here 👈

Description: Founded in 2006 by René Lacerte, Bill.com provides cloud-based software for small and medium businesses to pay vendors, approve bills, and collect money from customers. Additionally, Bill.com services accounting firms (over 70+ of the top 100 accounting firms) by helping them grow their book of business by automating bookkeeping tasks on behalf of customers. Banks also use Bill.com to provide their customers with a digital solution around cash flow management. The business also pitches itself as scaling with growing mid-size businesses like Hashicorp.

Pay Bills (Account Payable): Bill.com solves the pain point of customers having to manually send physical checks to pay for bills or track invoices and bills in filing cabinets. The company provides customers the option of paying via ACH, physical check or through a virtual credit card and if its an international vendor, Bill.com waives the international wire transfer fee.

Approval Workflow: Company's product can scan and digitize invoices in PDF and automatically generate a bill that kicks off the approval process by notifying the person who needs to approve the bill or invoice.

Get Paid (Account Receivable): Business also enables SMBs to send digital invoices to customers and sends automatic reminders to for customers to pay.

ROI: The company claims to have cut down the processing time of paper bills and invoices for a customer from 3 days a month to 1 hour and to help customers get paid 2x faster. In some instances, customers claim to have saved on not having to hire a full-time accounts payable person given the 2,000+ bills they receive in a year.

Business Model: Bill.com makes most of its money from subscription -- business owners pay $40-$100/user/month-- and transaction fees from ACH processing, checks or invoices mailed, virtual card payments, etc.

Go-to-market: Company acquires SMBs directly via online channels, word of mouth and trade shows. Additionally, Bill.com acquires customers indirectly via partnerships with 70+ of the top 1000 accounting firms which then introduce Bill.com to their clients.

Competition: Bill.com has various competitors that go after SMBs from larger enterprises like SAP, Sage Intacct, and Netsuite but also startups like Expensify that focus mostly on receipt and expense management (and not necessarily invoices). The accounting software tools like Freshbooks, Xero, and Quickbooks also provide some sort of AP and AR management but don't seem to act as direct competitors.

Strengths

👏Growth: 8th fastest-growing Public software company at 57% YoY and $140m revenue run rate (quarter revenue *4). Note the revenue isn't necessarily recurring software.

👏Low Cash Burn: the business consumed nearly $190m of capital to get to $140m revenue run rate which is ok from a capital efficiency perspective and most recently is -4% FCF which is effectively cash flow break even.

👏Gross Margins: margins are ~74% which is good but not necessarily amazing.

Weaknesses

🤷♂️Payback Period: While we have Bill.com as 2nd lowest payback period at 10 months using our 1/CAC Ratio methodology but the company does explicitly note that the average payback period in 2018 was 15 months which is good but not best in class for a business servicing SMBs.

🤷♂️Net Dollar Retention: Moderate net dollar retention at 110%. Understandably Bill.com is going after SMBs unlike the other high growth enterprise software companies

🤷♂️High Valuation: Business is trading for 13.1x EV/NTM ARRR which is in the middle of the pack for high growth software companies despite not necessarily having best in class NDR, payback period, or growth

🤷♂️Older Business: The company has been around since 2006 (versus the 2019 IPO class, the median founding date was 2010) and took nearly 13 years before going public. One worries that there may be a new up and coming product like Brex that may grab market share from Bill.com as companies like Brex move payments from ACH and invoices to credit cards.

Overall: Bill.com is a software company that's moving SMB payments online and growing quickly. However, the valuation is quite rich relative to peers and doesn't have exceptional business metrics.