Public Comps - Nov '19 SaaS Valuation 🔥

Public Comps - Nov '19 SaaS Valuation 🔥

Alteryx teardown and SaaS Valuations in Nov '19

From Jon and Howard

Thank you for continuing to be Public Comps customers! We will be sending regular content on SaaS earnings & S-1 teardowns and analysis.

We use emojis in our writing as we believe it makes SaaS metrics & analysis more fun

Reminder Public Comps = easiest & fastest way to get SaaS Benchmarks for Public SaaS Companies The best 🤯SaaS builders & investors use Public Comps to get SaaS metrics & analysis.

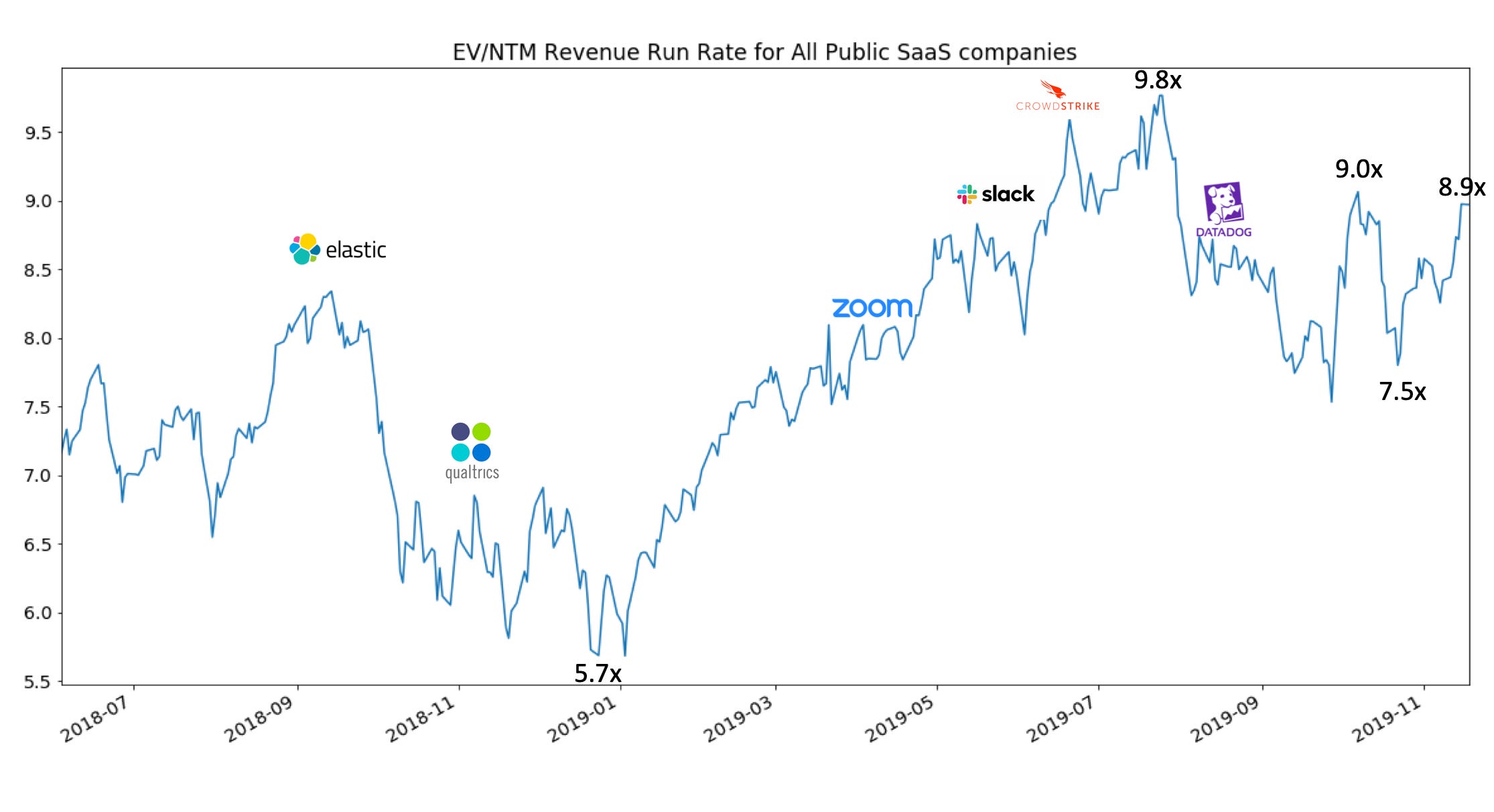

Public SaaS Valuations - November 18th, 2019

We look at Enterprise Value/Next-Twelve-Month ARR because SaaS companies can typically grow quickly (>40%) so we want to factor in the growth by looking at revenue on a forward basis.

SaaS valuations have been a rollercoaster in the last 18 months.

We had the floodgates of SaaS IPOs in 2018 with Dropbox, Zscaler, Docusign, Elastic, Qualtrics, and others go public. We had the peak of EV/NTM ARR at 8.3x Q3 '18 and then falling nearly 32% to 5.7x in the winter of 2018.

And then the happened all over again. SaaS valuations climbed to nearly 9.8x in July 2019 buoyed by the successful IPOs of two 100%+ YoY growth companies in Zoom and Crowdstrike.

The SaaS multiples then came crashing down. A Morgan Stanley analyst was worried that Workday would see a steeper deceleration in its Human Capital Management SaaS business and that there was going to be a more difficult software spending environment in 2020. There was a broader SaaS market sell-off.

Today we're back at 8.9x EV/NTM ARR -- not too far off from the peak in October '19.

In the last few weeks:

Datadog just reported that their growth accelerated from 82% YoY in Q2'19 to 88% YoY growth in Q3'19 at $384m ARR.

AWS is at $36b annualized revenue run rate (quarterly revenue*12) and growing 35% in Q3'19 down from 45% YoY in Q3'18 (77% growth persistence)

Azure is growing 59% YoY Q3'19 down from 75% YoY in Q3'18 (78% growth persistence)

My take is that while the cloud vendors in AWS and Azure are slowing down (if standalone businesses, their growth is still in the top 75th percentile of high growth SaaS!), there are still a lot of SaaS companies that will continue to accelerate like Datadog or grow with high persistence (>85%). Alteryx is a great example.

Alteryx Earnings Teardown

Alteryx is a pretty special business. You can look at Alteryx historical financials here and their most recent earnings here

Here's how Alteryx looks vs the other top 10 fastest growing SaaS:

Alteryx Summary

Alteryx is the 6th fastest growing Public SaaS company at $400m ARR with 65% YoY growth

🤷♂️Yet, the stock price is down ~50% last 3 months ($142 in Sept '19 to $98 in Nov '19)

Description: Alteryx = no-code + self-service analytics tool for data analysts and data scientists to join, clean and prepare data for analysis and visualization.

Business teams at BCG, Nike, Facebook, Amazon, and Netflix use Alteryx to clean & process large datasets that can't be analyzed in just Excel so the teams can get insights from their data in minutes versus weeks

Competition: Competitors include older incumbents like IBM, Microsoft, Oracle, SAP, SAS, Microstrategy, and TIBCO that offer some data preparation or analytics tools . Upstart data prep competitors include Dataiku (raised $100m from ICONIQ in Dec '18), Trifacta (raised $100m in Sept '19), Paxata (raised $61m to date), Knime (Opensource), etc . It seems like Alteryx's main competitor are really business analyst cleaning data themselves manually in Excel 🤦♀️

Market: 47m spreadsheet users (by far the largest market in the "Data Tooling" space). Alteryx estimates its market to be ~$50b.

Here's what to like

#6 Fastest-Growing Public SaaS at 65% YoY.

Growth accelerated from 59% YoY Q3'18 to 65% YoY Q3'19 (110% Growth Persistence)

>5,600 customers and adding new logos at 30%+ YoY

#5 Highest Net Dollar Retention at 132% — successful land & expand model and rarely losing customers.

#1 lowest payback period at 7.5 months. Suggests there's still a lot of room to grow?

#2 highest Last-Twelve-Month Free Cash Flow at 6.2%

#1 Gross Margins among all SaaS at 90%

#2 lowest SaaS valuation (9.7x EV/NTM Revenue Run Rate)

#1 lowest SaaS valuation when considering gross margin (10.7x EV/NTM Gross Profit Run Rate)

Here's what not to like

Been around since 1997 (!) ~22 years

Criticism that visualization of analytics is not great ... but Alteryx does partner up with Tableau

⛹️♂️Can Alteryx continue to innovate on new products beyond data prep or through acquisitions like feature engineering startup Feature Labs?